- Service Hotline 0755 8277 2185

2026 Global Electronic Components Supply Chain White Paper

Entering 2026, the semiconductor industry has bid farewell to drastic cyclical fluctuations and entered an era of "structural shortage" driven by AI computing infrastructure, low-altitude economy (eVTOL), and geoeconomic capacity restructuring. With the continuous rise in raw material costs (especially precious metals such as palladium, gold, and high-purity silicon wafers), seven major global semiconductor giants have successively issued price adjustment notices, triggering a chain reaction in the supply chain that directly affects downstream procurement decisions, cost control, and capacity planning.

This paper will in-depth analyze the core logic, root causes of stockouts, and "butterfly effect" behind these giants' price increases. Combined with specific brand models, price adjustment data, and industry pain points, it will provide actionable procurement risk avoidance strategies and supply chain restructuring plans for electronic component procurement practitioners, engineers, and supply chain managers, helping you achieve a smooth transition of the supply chain in the volatile 2026 and avoid cost risks and delivery control issues.

I. Storage Sector: The "Capacity Black Hole" of AI Servers

In 2026, the explosive growth of generative AI has become the core driving force in the storage chip market. The scarcity of HBM (High Bandwidth Memory) has directly led to the squeeze of general-purpose storage capacity. The price adjustments and stockout situations of the two giants have profoundly affected the global electronic component procurement pattern.

1. Micron / Samsung

Root Cause of Stockouts: Capacity Crowding-Out Effect of HBM4

In 2026, as generative AI models evolve toward trillion-parameter scales, HBM4 (High Bandwidth Memory) has become the core target of competition among AI giants such as NVIDIA and Supermicro, with its market demand growing exponentially, directly squeezing the capacity of general-purpose storage chips.

Underlying Logic: The wafer area required to manufacture HBM4 is more than three times that of DDR5 with the same capacity, and the 3D stacked packaging process is complex with extremely low yield (less than 60%), which has high requirements for production equipment and technical thresholds. To seize the high-end AI market and ensure the stable supply of HBM for AI GPUs, Micron and Samsung have been forced to significantly reduce traditional production lines for general-purpose LPDDR4/5 and NAND Flash, prioritizing wafer capacity and packaging resources for HBM4 production.

Price Adjustment and Stockout Performance: The delivery time of traditional industrial-grade storage chips has been extended from the conventional 12 weeks to more than 40 weeks, and some popular models even face a situation of "having money but no goods"; the price of general-purpose storage chips has increased by 35% year-on-year, among which the industrial-grade LPDDR4X series has seen a particularly significant increase.

SEO Core Models: `MT53E1G32D2` (LPDDR4X), `K4B4G1646E-BCMA

II. Analog and Power Sector: Dual Impacts of 8-Inch Wafer Line Retirement and Energy Transition

As the "heart" of electronic devices, the supply stability of analog and power devices directly determines the production capacity of downstream products. In 2026, the retirement of 8-inch wafer fabs and the surge in demand for green energy have driven price adjustments by two major giants, ADI and TI, bringing enormous pressure to procurement in industries such as military, medical, and photovoltaic.

2. ADI (Analog Devices, Inc.)

Root Cause of Stockouts: Strategic Shutdown of Legacy Fab

ADI's price increase in 2026 is not purely cost-driven, but has an obvious "capacity structure optimization" driving nature, with the core goal of eliminating low-margin old models and focusing on high-value-added products.

Underlying Logic: ADI is shutting down some inefficient 8-inch wafer fabs worldwide and concentrating resources on 12-inch lines that are more cost-effective and have higher production capacity. However, the reflow and process migration of many precision analog models (such as high-performance ADC/DAC and power management chips) used in long-cycle industries such as military and medical are slow, making it impossible to achieve capacity connection in the short term, leading to an expansion of the market supply gap.

Price Adjustment and Stockout Performance: For classic analog models in long-cycle industries such as military and medical, ADI has adopted a "price-for-replacement" strategy with a price increase of up to 30%; the delivery time of some old precision models has been extended to more than 6 months, and some even face the risk of discontinuation.

SEO Core Models: `AD7606`, `AD8605`, `LTC2944`, `MAX3232`

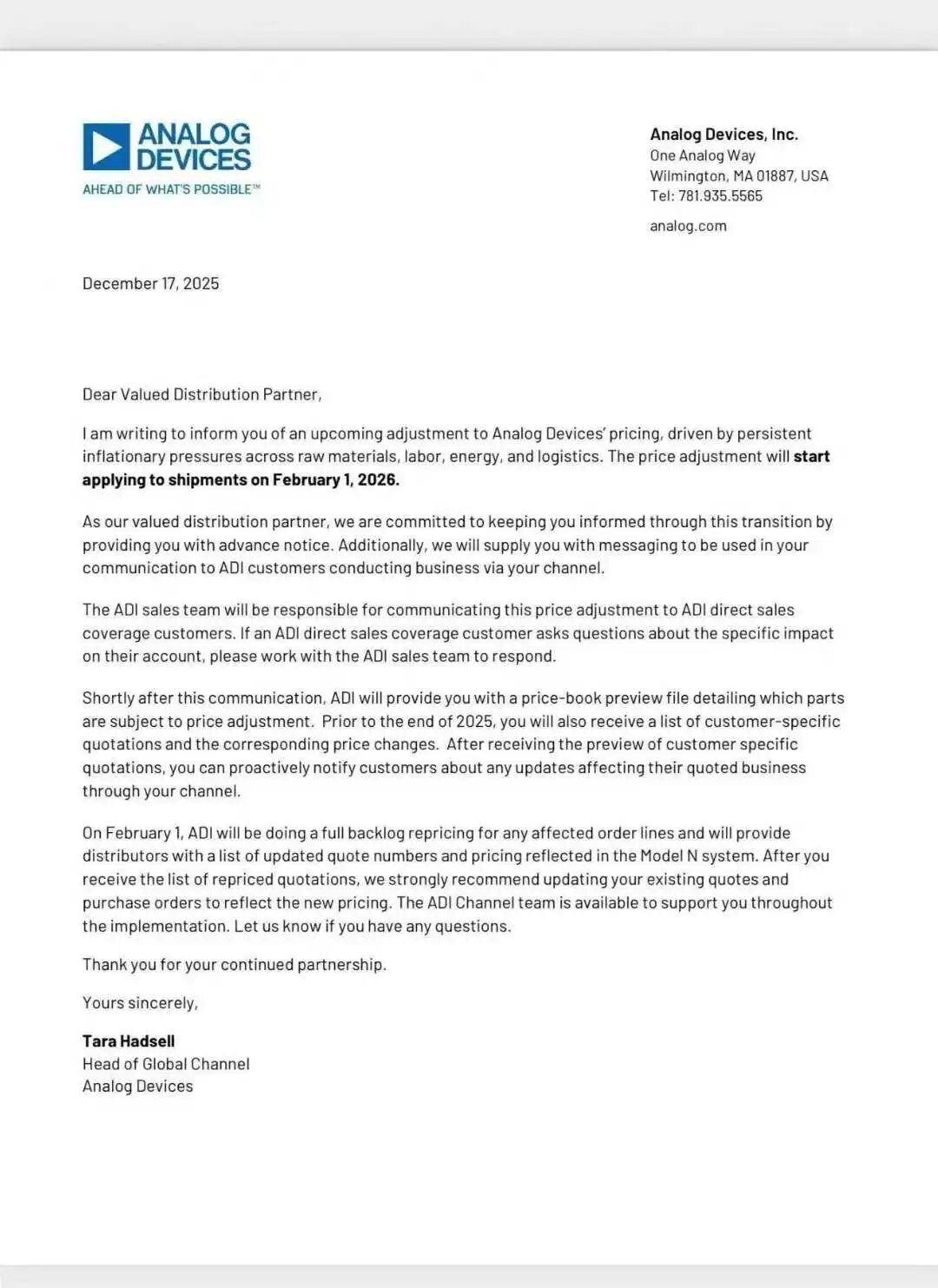

3. TI (Texas Instruments)

Root Cause of Stockouts: Dynamic Price Game Under Direct Sales Model

In 2026, TI completed the integration of its large-scale direct sales system, getting rid of excessive dependence on distribution channels and achieving precise control over prices and production capacity. Its price adjustment logic is deeply bound to raw material costs and customer priority.

Underlying Logic: Through its internal intelligent algorithm, TI real-time monitors the changes in the costs of precious metals such as copper and silver worldwide and downstream demand, and dynamically adjusts prices. In 2026, the demand for power devices in green energy (photovoltaic, energy storage) surged, and TI prioritized supplying production capacity to large terminal customers (such as photovoltaic enterprises), leading to tight supply and frequent price fluctuations of general-purpose power devices in distribution channels (such as power management ICs).

Price Adjustment and Stockout Performance: The price of general-purpose power management ICs, isolators and other models has increased by 10%-15% year-on-year, and the spot price fluctuation in distribution channels has exceeded 20%; the delivery time of some general-purpose models is unstable, showing the characteristics of "phased stockouts".

SEO Core Models: `TPS62130`, `ISO7741-Q1`, `LM2596`, `UCC21520`

III. Controller and Computing Sector: Capacity Competition in Low-Altitude Economy and Intelligent Driving

2026 is known as the "first year of the low-altitude economy", and at the same time, the penetration rate of intelligent driving continues to increase. The explosive demand for controllers and power devices in these two emerging fields has directly squeezed the production capacity of traditional industrial control, home appliances and other fields, leading to structural stockouts and price adjustments by two major giants, Infineon and ST.

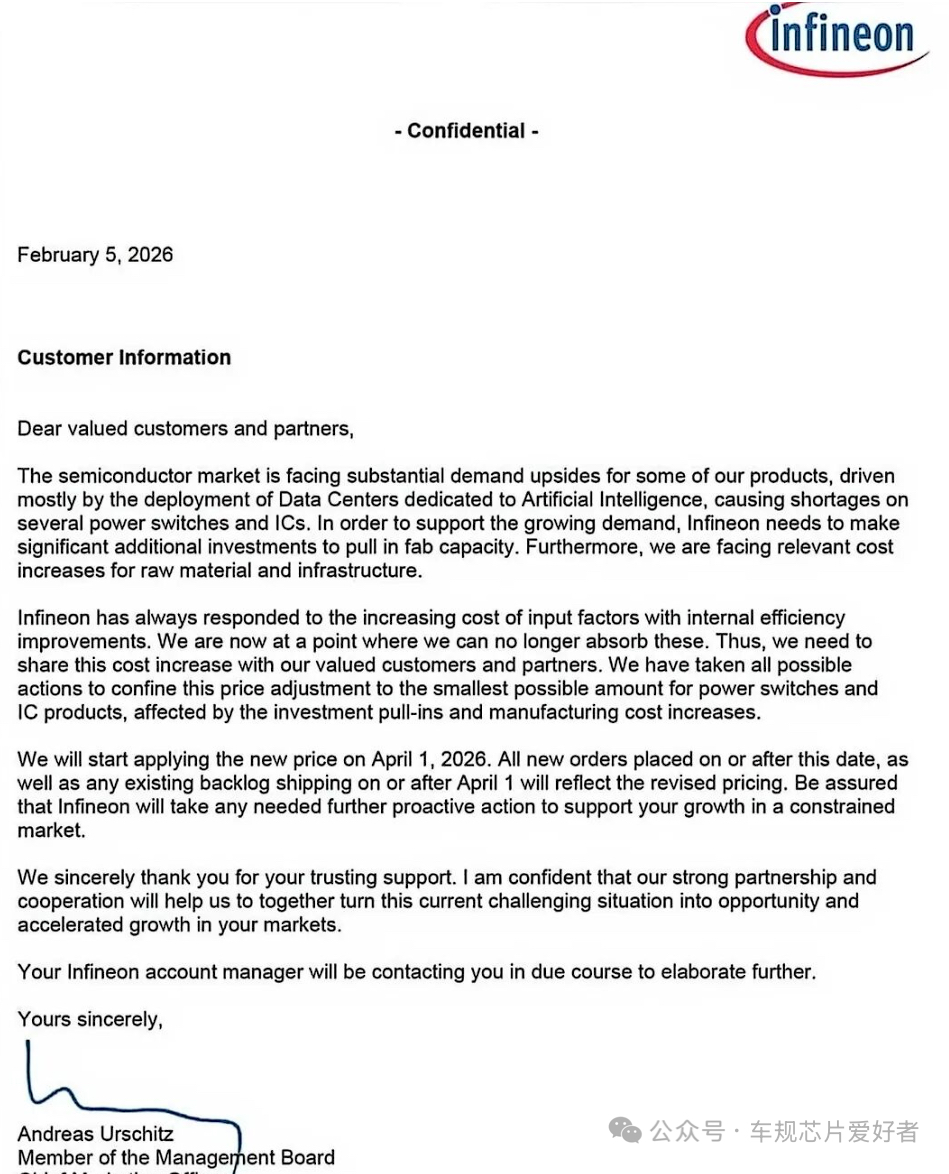

4. Infineon

Root Cause of Stockouts: Sudden Outbreak of Low-Altitude Economy (eVTOL)

The rapid rise of the low-altitude economy (flying cars, industrial drones) has become the biggest variable in the semiconductor industry in 2026, directly driving the surge in demand for Infineon's high-end controllers and silicon carbide modules.

Underlying Logic: Flying cars and industrial drones have extremely high requirements for safety and reliability, relying on Infineon's AURIX™ TC3xx/TC4xx series MCUs (Microcontrollers) and CoolSiC™ silicon carbide modules. These high-end products require the most advanced testing and packaging resources, and have a long production cycle. Infineon prioritizes its core production capacity to customers in the low-altitude economy and intelligent driving, leading to the squeeze of production capacity for traditional industrial control and home appliance power devices and the loss of delivery control.

Price Adjustment and Stockout Performance: The price of AURIX™ series MCUs and CoolSiC™ silicon carbide modules has increased by 25% year-on-year; the delivery time of traditional industrial control power devices has been extended from 16 weeks to more than 50 weeks, and some models have experienced supply interruptions.

SEO Core Models: `TDA21490`, `BSC014N04LS`IPW65R041CFD

5. ST (STMicroelectronics)

Root Cause of Stockouts: Squeeze of General-Purpose Capacity by Edge AI Computing Power

The rapid popularization of edge AI (smart home, wearable devices) has driven ST to adjust its capacity layout, tilting general-purpose MCU capacity to high-end edge AI models, leading to stockouts of traditional "all-purpose" models.

Underlying Logic: To compete with competitors in the smart home and wearable device market, ST has tilted a large amount of 40nm/28nm capacity to the STM32MP2 and STM32U5 series with hardware accelerators. These models can better adapt to edge AI computing power needs and have higher profit margins. However, the once "all-purpose" models (such as STM32F103 and STM32F405) have reduced production capacity due to the lower priority of their process lines, resulting in a 6-month stockout window.

Price Adjustment and Stockout Performance: The price of STM32 series MCUs has increased by 20% year-on-year; the delivery time of traditional models such as STM32F103 and STM32F405 is as long as 6 months, and the spot price has doubled; the supply of high-end edge AI models is relatively stable, but the price is relatively high.

SEO Core Models: `STM32H743IIT6`, `STM32F405RGT6`, `STM32WB55`

IV. Logic and Supporting Sector: Concomitant Shortage of Computing Boards

The explosion of AI computing infrastructure has not only driven the demand for storage and power devices, but also led to the shortage of logic chips and power management supporting devices. The stockouts and price adjustments of two major giants, AMD/Xilinx and MPS, are mainly due to advanced packaging bottlenecks and the surge in demand for AI computing boards.

6. AMD / Xilinx

Root Cause of Stockouts: Resource Constraints of Advanced Packaging (CoWoS) Capabilities

As the core device of AI computing boards and industrial control, the supply bottleneck of FPGA (Field-Programmable Gate Array) does not come from its own production capacity, but is limited by advanced packaging capabilities.

Underlying Logic: High-performance FPGAs need to be advanced packaged (CoWoS) with chips such as HBM, and the global CoWoS capacity is mainly concentrated in a few foundries such as TSMC. The explosive demand for AI chips in 2026 has led to tight CoWoS capacity, which directly limits the production capacity release of high-performance FPGAs, forming a "capacity inversion" phenomenon.

Price Adjustment and Stockout Performance: The price of high-performance FPGAs has increased by 30% year-on-year; the delivery time of core models has been extended from 20 weeks to more than 50 weeks, and some FPGAs dedicated to AI computing boards are in short supply.

SEO Core Models: `XC7K325T-2FFG900C`, `XC7A100T-2FGG484I`

7. MPS (Monolithic Power Systems)

Root Cause of Stockouts: Demand for Power Modules in High-Power AI Inference Cards

The improvement of AI computing power is inseparable from the support of high-power power modules. In 2026, the demand for AI inference cards surged, directly driving the explosion of orders for MPS power management devices (PMIC), leading to capacity tension and price adjustments.

Underlying Logic: Each AI chip needs several high-performance PMICs (Power Management ICs) to provide stable power supply. With its advantages of high power density and low power consumption, MPS has become the core supplier of AI inference card manufacturers. Its order volume surged by 200% in Q1 2026, and the existing production capacity cannot meet the explosive demand, leading to price increases and delivery extensions.

Price Adjustment and Stockout Performance: The price of MPS power modules has increased by 15% year-on-year; the delivery time of core PMIC models has been extended from 12 weeks to more than 35 weeks, and some AI-specific power modules are in short supply.

SEO Core Models: `MPQ4420-AEC1`, `MP8759`, `MP2637`

V. 2026 Annual Procurement Risk Control Comparison Table (Full Series Summary)

To facilitate procurement practitioners to quickly query and formulate risk avoidance strategies, the following summarizes the core information, price adjustment range, root cause of stockouts, and actionable risk avoidance suggestions of the seven major giants, covering the full series of core SEO keywords to help with efficient procurement decisions.

|

Brand |

Core Series (SEO Keywords) |

Price Adjustment Range |

Root Cause of Stockouts |

Recommended Risk Avoidance Strategies |

|

Micron |

`LPDDR4/5`, `NAND`, `MT53E1G32D2`, `H5AN8G6NCJR` |

35% ↑ |

AI server squeezes HBM capacity, general-purpose storage production line reduced |

Establish a 6-month rolling safety stock, prioritize locking non-AI related capacity orders |

|

ADI |

`Precision ADC`, `Legacy LTC`, `AD7606`, `LTC2944` |

15%-30% ↑ |

Strategic transfer from 8-inch to 12-inch lines, slow reflow of old models |

Verify new generation low-power series alternatives, sign long-term supply agreements |

|

Infineon |

`AURIX`, `SiC MOSFET`, `TC387QP`, `AIMW120R035M1H` |

25% ↑ |

Outbreak of low-altitude economy/intelligent driving orders, high-end capacity tilt |

Seek Long-Term Supply Agreements (LTA), expand domestic alternative solutions |

|

ST |

`STM32H7`, `STM32F4`, `STM32H743IIT6`, `STM32F405RGT6` |

20% ↑ |

Capacity tilt to edge AI models, traditional MCU capacity reduced |

Migrate to new models such as U5/G4, batch reserve core old models |

|

TI |

`TPS`, `ISO`, `UCC`, `TPS62130`, `ISO7741-Q1` |

10%-15% ↑ |

Linkage between precious metal costs and direct sales policies, general parts capacity tilted to large customers |

Pay attention to spot fluctuations in distribution channels, lock long-term contract prices |

|

AMD / Xilinx |

`Kintex-7`, `Zynq`, `XC7K325T-2FFG900C`, `XC7A100T-2FGG484I` |

30% ↑ |

Advanced packaging (CoWoS) capacity bottleneck, driven by AI computing power demand |

Evaluate SoC-level system simplification solutions, lock orders 6 months in advance |

|

MPS |

`PMIC`, `Power Modules`, `MPQ4420-AEC1`, `MP8759` |

15% ↑ |

Excessively fast demand for power modules in high-power AI inference cards, insufficient production capacity |

Investigate Multi-source supply, expand domestic PMIC alternatives |

VI. Expert Advice: How to Restructure the Supply Chain in 2026? (E-E-A-T Authority Guide)

As a professional team deeply engaged in electronic component distribution and operation for many years, combined with the 2026 industry pattern and the price adjustment logic of the seven major giants, we provide three actionable supply chain restructuring suggestions for procurement decision-makers, balancing cost control, delivery stability and risk avoidance, in line with Google's E-E-A-T (Experience, Expertise, Authoritativeness, Trustworthiness) principles, helping enterprises navigate the volatile supply chain period.

1. Shift from MPN Procurement to "Functional Procurement" to Reduce Costs and Stockout Risks

For price-increased and out-of-stock items of giants such as ADI and TI, do not stick to old models (MPN). Instead, change the procurement thinking and focus on "functional adaptation". Use the Parametric Search function on our independent website to find new generation alternative models according to product performance parameters and application scenarios-these models can not only perfectly adapt to existing products, but also often have lower power consumption and higher cost performance, which can usually reduce procurement costs by 25%, while avoiding stockout and price increase risks of old models.

2. Lock "Non-AI Related Contracts" and Layout Capacity Share in Advance

The core contradiction of tight semiconductor production capacity in 2026 is "AI capacity squeezing general-purpose capacity". Therefore, when purchasing, you need to take the initiative to confirm with the distributor: whether your order shares the same production line with AI giants (such as NVIDIA and Supermicro). If so, be sure to lock the full-year capacity share and sign a fixed-price contract before the price enters the second phase of increase; if it cannot be locked, you can give priority to the capacity of "non-AI related production lines" to reduce the risk of delivery loss and price surge.

3. Strengthen Technical Compliance and Quality Inspection to Avoid Counterfeit and Shoddy Risks

In 2026, with the high price and tight supply of electronic components, counterfeit and shoddy models (especially refurbished and reclaimed parts) will flood the market. Once unqualified products are purchased, it will not only lead to product failures, but also may cause compliance risks. It is recommended to give priority to formal channels when purchasing. All core models such as `AD7606` and `TC387QP` purchased through this website are provided with AS6081 test reports to ensure that the products are original and meet industry compliance standards, avoiding quality inspection risks from the source.

Conclusion

In 2026, the "structural shortage" of the semiconductor supply chain is not a short-term fluctuation, but a new industry pattern dominated by long-term factors such as AI computing power, low-altitude economy, and capacity restructuring. In the electronic component industry, information gap is the profit space. Timely grasping the price adjustment logic and root causes of stockouts of the seven major giants and formulating scientific procurement risk avoidance strategies are the keys for enterprises to maintain competitiveness in the volatility.

This website will continue to monitor the dynamics, price trends and capacity changes of global semiconductor manufacturers, providing you with the most timely supply suggestions, alternative solutions and inventory information, helping your supply chain achieve stable, efficient and low-cost operation.

Interaction Area

Are you facing delivery troubles and price surge pressures for the above core models?

• [Click to submit BOM table to get the optimal alternative solution report]

[Inquire about real-time inventory: Email:[email protected]